Parents

Research

Mar 18, 2026

Beef is on the Menu: The Cattle Industry in the Coming Years

Andrew Z

Research Fellow

We Have the Meats

Cattle production is one of the most important segments of American agriculture and consistently represents the largest share of total US farm cash receipts. The industry is typically divided into two main stages: cow-calf operations and cattle feeding (feedlots). Cow-calf producers focus on breeding herds and raising calves. Calves are usually born in the spring and weaned after about 3 to 7 months. After weaning, some animals are kept as replacements to maintain the breeding herd, while most are sold into the broader beef production system. These ranches often operate on open grasslands and pasture, much of which is not suitable for growing crops, making cattle an efficient way to turn otherwise unusable land into food.

Once calves leave the ranch, they enter the feeding system, where the goal shifts from raising animals to maximizing weight gain and meat quality. Young cattle may spend several months grazing or being “backgrounded” on forage and grain before moving to feedlots. In feedlots, cattle are placed on carefully designed, high-energy diets that help them gain weight quickly and consistently. This final stage prepares animals to meet USDA quality grades such as Prime, Choice, and Select, which determine the price processors and retailers can charge.

Economically, cattle production is enormous. In 2024, it accounted for roughly 22% of total U.S. agricultural cash receipts, or about $515 billion across all commodities. Domestic beef demand remains strong and stable as well, with Americans consuming roughly 28 to 29 billion pounds into 2026.

Although beef production is a mature and well-established industry in the United States, there are still signs of excitement. In particular, three trends should warrant the attention of retail investors: the cattle cycle, which drives swings in supply and prices; the development of new feed and methane-reducing additives that improve production concerns; and growing export demand that expands markets for US beef worldwide.

It Comes and Goes

Beef production follows a natural boom-and-bust pattern known as the cattle cycle, and this cycle is one of the most important drivers of profitability of cattle producers. Given cattle take years to raise, producers cannot instantly increase supply when prices rise. Instead, herd sizes expand and contract slowly over time, creating predictable periods of shortage followed by oversupply. These delayed adjustments cause prices to swing for years at a time.

Historically, the cattle cycle lasts about eight to 12 years. The cycle often begins with undersupply, when herds are small and there is less beef available on the market. With fewer animals heading to slaughter, wholesale and retail beef prices rise. Higher prices then encourage ranchers to expand production. Instead of selling female calves, known as heifers, producers keep them for breeding. However, expansion takes time as a heifer must grow for about two years before having her first calf, and that calf then needs roughly 18 months to reach slaughter weight. In total, it can take three to four years before additional beef actually reaches grocery stores. During this lag, supply remains tight and prices can stay elevated for multiple years.

Eventually, those retained calves mature and enter feedlots, leading to oversupply. More cattle reach slaughter at once, beef production jumps, and prices fall. Producers then reduce breeding herds, sending more cows to slaughter in the short term. This temporarily increases supply and keeps prices low, but over time it reduces the number of breeding animals and sets up the next shortage. The result is a repeating pattern of rising and falling inventories that drives long-term price cycles.

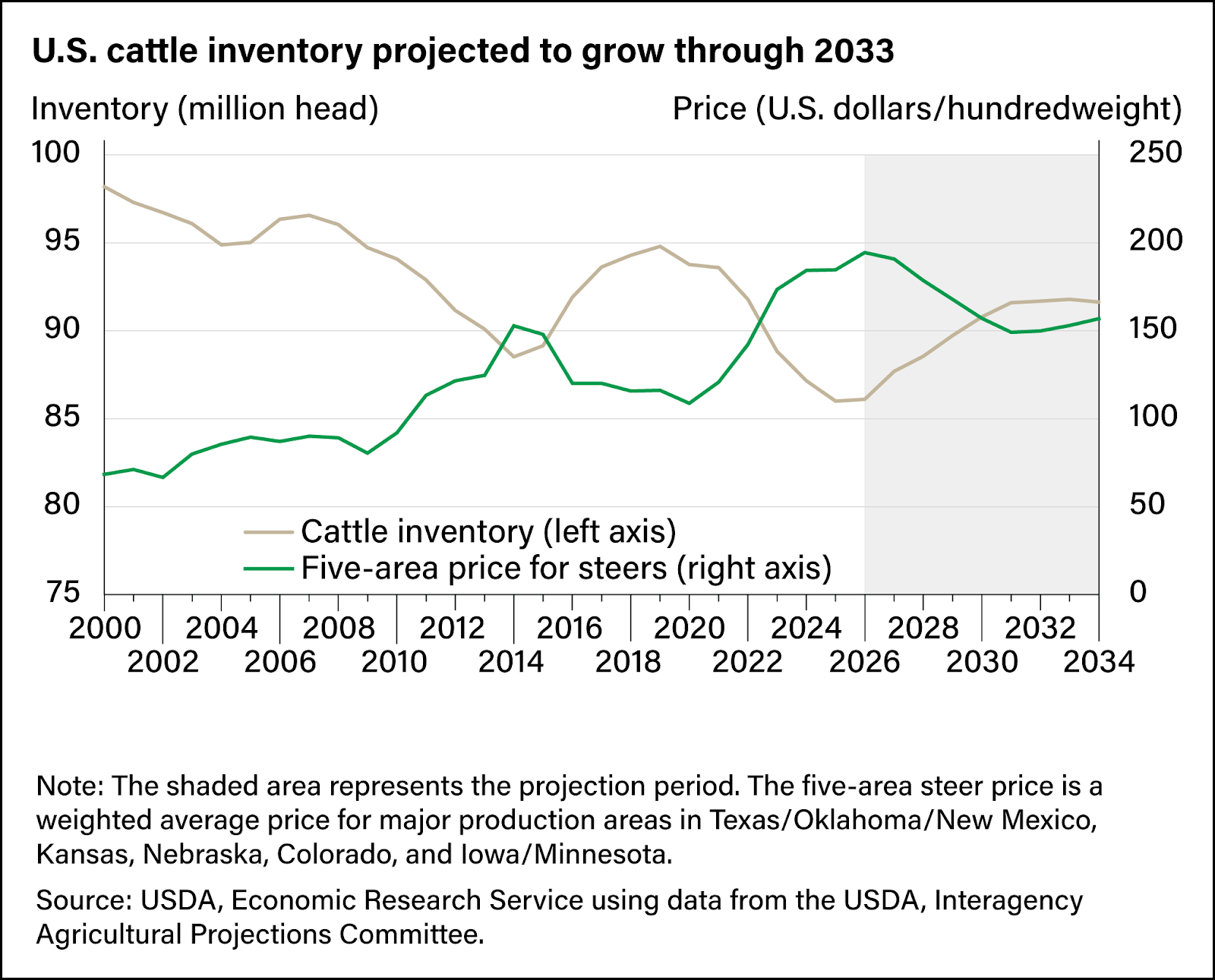

Source: USDA

Today, the US cattle cycle appears to be firmly in a tight-supply phase. After a recent peak in 2019, national cattle inventories have declined and are projected to reach a multidecade low in 2025, with total inventory around 86 million head, the lowest level since 1951. From there, inventories are expected to rebuild gradually through 2033, reaching about 91.8 million head, before edging down slightly to 91.6 million head in 2034 as the next shift in the cycle begins. Tight supplies are already pushing prices higher. In 2026, low cattle numbers are projected to drive the five-area steer price to a record $196.49 per hundred pounds, before falling to $150.65 by 2031 and then rising again to about $158.47 by 2034 as the next cycle unfolds. These multi-year price swings directly affect the revenues and margins of cattle producers and processors.

Importantly, higher prices have not meaningfully weakened consumer demand. In 2024, shoppers spent over $40 billion on fresh beef alone, accounting for more than half of all fresh-meat sales. From beginning to mid-2025, retail beef prices averaged $6.94 per pound, up 5.8% year over year, yet demand has remained resilient, and this is even considering that chicken prices rose only 2.9% and pork prices only 1.2%. Even as prices climbed, both value and volume held up: fresh beef retail dollar sales increased 12.5% while volume rose 6.3%. Within categories, steak and roast dollar sales grew 13.7%, pounds sold increased 7.8% and 9.3%, and ground beef posted a 4.4% increase in volume. Rather than abandoning beef, consumers tend to trade between cuts, switching to more affordable options like ground beef while staying within the category.

With inventories near historic lows and prices elevated, while demand remains steady in the tens of billions of pounds, the industry benefits from both constrained supply and stable consumption.

Yep, Cows Fart

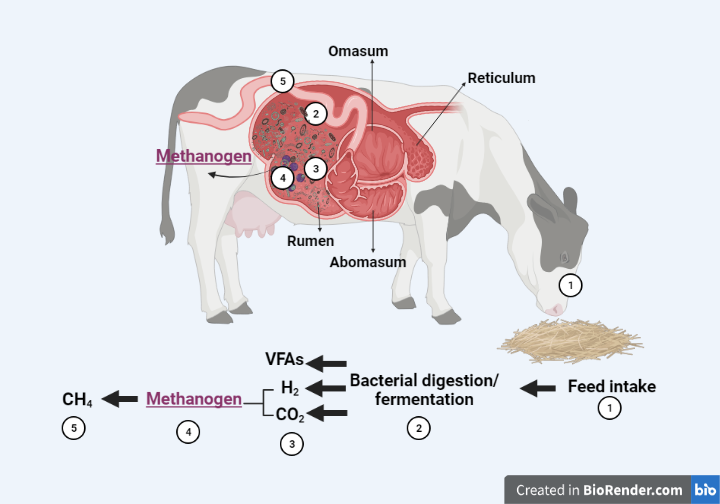

While beef remains one of America’s most popular proteins, it also faces a growing challenge: its environmental footprint. Researchers estimate that the production and consumption of beef account for roughly 3.8% of total US greenhouse gas emissions. A large portion of this comes from methane, a greenhouse gas that traps heat much more strongly than carbon dioxide. In fact, methane has about 28 times the warming potential of CO2. Cattle naturally produce methane as part of digestion. Because cows are ruminants, they break down tough plant material like grass using microbes in their stomach. During this process, special microorganisms called methanogens create methane as a byproduct, which is released into the atmosphere when cows burp. On average, one cow can produce roughly 200 pounds of methane per year, and livestock, mostly cattle, account for about 25% of US methane emissions from human activities.

Source: University of Wisconsin

Fortunately for the industry, new technologies known as feed additives are emerging as a practical solution, helping cattle produce less methane while maintaining growth and productivity. Feed additives are ingredients added in small amounts to cattle feed that do not provide direct nutrition but instead improve how the animal’s body functions. Some additives alter the microbes in the rumen to disrupt methane production, allowing cattle to use more of their feed for growth instead of losing energy as gas. In other words, cattle can grow just as fast, or sometimes faster, while emitting less methane. Because methane represents wasted energy, reducing it can actually make feed conversion more efficient.

Two of the most widely studied options are 3-nitrooxypropanol (3-NOP) and a red seaweed called Asparagopsis taxiformis. Trials have shown that 3-NOP can cut methane emissions by 30-50%, while adding small amounts of seaweed supplements has reduced emissions by almost 40% in some grazing cattle, all without harming animal health or weight gain. Furthermore, these reductions are very feasible as they can be achieved with very small doses, often less than 1% of a cow’s daily feed intake, meaning the additives can be incorporated into existing operations with minimal disruption.

Reducing methane can help cattle producers stay ahead of tightening regulations and meet sustainability standards set by governments, retailers and food companies. At the same time, improving digestion means cattle convert more feed into weight gain instead of losing energy as methane, lowering feed costs.

Around the World

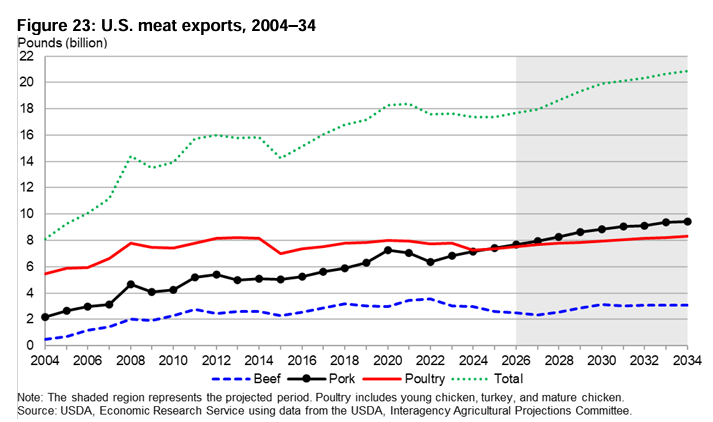

A major component to the profitability of the US cattle industry lies beyond America's borders. Over the past several decades, exports have become a major and increasingly important source of demand. Exports now represent a large share of total production. In the 1980s, US beef exports were limited and inconsistent. Fast forward to 2024, and exports accounted for nearly 14% of total US beef production. Export markets contributed about $415.08 in value per head of fed cattle slaughtered, one of the highest levels on record. In other words, selling beef overseas doesn’t just add volume — it adds profitability.

Growth has been especially strong in regions with established trade agreements and rising middle-class incomes. Between 2020 and 2024, the fastest-growing markets by volume included the Caribbean, China, Central America, Mexico, and the Philippines. In 2023, exports to the Caribbean and Central America reached record highs, and shipments to Mexico were the strongest since 2009. Today, just six key markets — Korea, China, Japan, Mexico, Canada and Taiwan — account for roughly 86% of total US beef export value. These countries increasingly rely on imported beef as their populations grow wealthier and diets shift toward higher protein consumption.

Looking forward, global trade is expected to expand further. Worldwide beef demand is projected to grow over the next five years, mainly supported by rising consumption across Asia and increasing imports from South American markets. In the second half of the decade, countries such as Vietnam, China, Malaysia, and the Philippines are expected to see continued per-capita consumption growth, which should increase their reliance on imported beef. During the 2026 to 2034 projection period, US beef exports are forecast to rise by about 22%, from 2.5 billion pounds to 3.1 billion pounds. Although Brazil is expected to remain the largest exporter globally and India second, the United States is projected to gain market share by increasing shipments later in the period while exports from Australia and the European Union decline. Accordingly, the future increase in exports will provide US cattle producers a clear opportunity to access more diversified demand and significant growth.

Source: USDA

What to Consider

Together, these trends bring enthusiasm to the cattle industry for investors. Tight inventories support stronger revenues, feed additives improve efficiency and reduce environmental risks and exports add new buyers and pricing power abroad. Investors may consider:

- Beef processors directly benefiting from higher cattle prices, exports, and operating leverage:

- Tyson Foods (TSN)

- JBS (JBS)

- Hormel Foods (HRL)

- Animal nutrition and feed suppliers positioned to gain from feed efficiency and additive adoption:

- Darling Ingredients (DAR)

- Archer-Daniels-Midland (ADM)

- Bunge Global (BG)

- Agricultural input providers supporting feed production and crop yields:

- CF Industries (CF)

- The Mosaic Company (MOS)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.